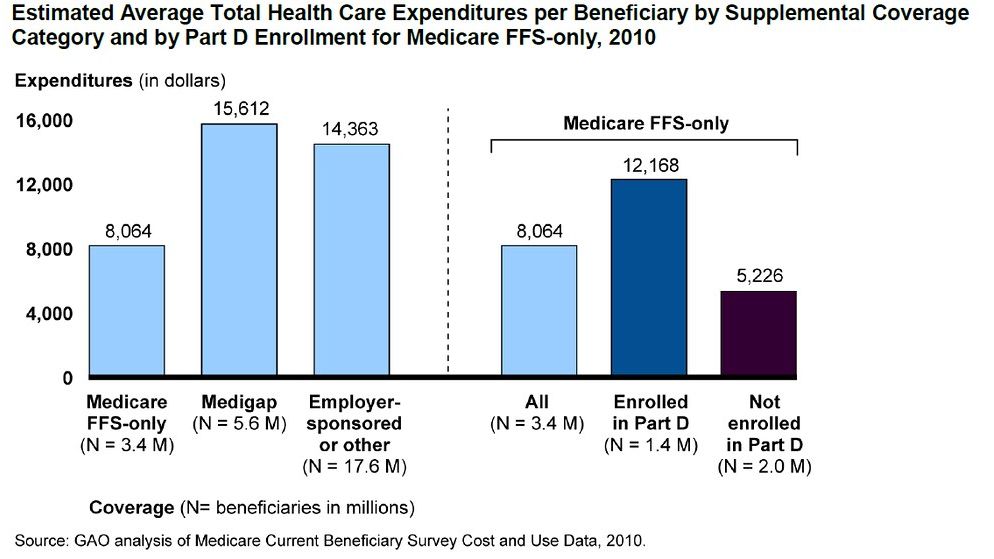

Turning 65 Medicare Checklist: Your Complete Step-by-Step Enrollment Guide – Image for illustrative purposes only (Image credits: Flickr)

Many adults reach their mid-sixties with questions about health coverage options. Medicare provides a federal framework that can help manage medical costs, yet missing key deadlines often leads to lasting financial consequences. A structured approach reduces confusion and supports informed decisions during this transition.

Recognize the Initial Enrollment Window

The first opportunity to join Medicare opens three months before the month of a person’s 65th birthday. Coverage can begin as early as the first day of that birthday month when enrollment occurs on time. Delaying beyond the seven-month window that follows usually triggers late penalties that continue for the rest of a beneficiary’s life. Planning ahead allows time to gather required documents such as a birth certificate and Social Security number. Individuals already receiving Social Security benefits are often enrolled automatically, while others must submit an application directly. Reviewing personal health needs during this period helps determine whether additional coverage beyond basic parts will be necessary.

Understand the Main Coverage Parts

Medicare divides benefits into distinct parts that address different types of care. Part A covers hospital stays and some skilled nursing services, while Part B handles outpatient visits, preventive screenings, and physician services. Most beneficiaries combine these two parts for broader protection. Part D adds prescription drug coverage through private insurers, and many people also consider a Medicare Advantage plan or a supplemental policy to limit out-of-pocket expenses. Each option carries its own costs and network rules, so comparing details prevents surprises once coverage starts. Official summaries from Medicare outline the differences clearly and remain the most reliable reference.

Complete the Checklist in Order

A practical sequence keeps the process manageable and avoids common oversights.

- Confirm eligibility and gather identification documents several weeks before the birthday month.

- Decide whether to enroll in Parts A and B during the initial window.

- Review prescription needs and compare Part D plans available in the local area.

- Evaluate whether a Medicare Advantage or Medigap policy fits expected medical usage.

- Submit the application through Medicare.gov or by phone and retain confirmation numbers.

- Set calendar reminders for future annual open enrollment periods each fall.

Following these steps in sequence supports timely activation of benefits and reduces the chance of gaps in coverage.

Monitor Ongoing Requirements

Enrollment does not end the need for attention. Annual reviews of drug formularies and provider networks help maintain suitable coverage as health circumstances change. Beneficiaries should also watch for notices about premium adjustments or plan updates that arrive each year. Staying informed through official Medicare channels ensures adjustments can be made during the appropriate windows without penalty. This ongoing vigilance protects both access to care and long-term budget stability.